The Nature of Economics

Matthew Williams

||8 min readCSEC EconomicsEconomic AgentsOpportunity CostPaper 01Paper 02PPFScarcitySection 1

Economics as a social science, scarcity and the central economic problem, free and economic goods, branches of economics, the three economic agents, opportunity cost, and the production possibility frontier.

Economics studies how people and societies make decisions when resources are limited but wants are not. That constraint — scarcity — is the starting point for everything else in the subject.

What is Economics?

Economics is a social science concerned with three things: how scarce resources are allocated, how wealth is created, and how goods and services are produced, distributed, and consumed. Because it studies human behaviour and interactions, it sits alongside other social sciences such as politics, history, and sociology.

The central economic problem is that resources are finite while human wants are unlimited. No society can ever produce enough to satisfy every desire, so choices must constantly be made. Economics analyses how those choices are made and what their consequences are.

Branches of Economics

| Branch | Focus |

|---|---|

| Microeconomics | Individual units: households, firms, and specific markets. Asks questions like: how does a firm set its price? What determines a worker's wage? |

| Macroeconomics | The economy as a whole. Asks questions like: why does inflation rise? How does government spending affect employment? |

Sections 1–4 of the CSEC syllabus cover microeconomics; Sections 5–8 cover macroeconomics.

Scarcity, Choice, and Opportunity Cost

Scarcity is the condition in which available resources are insufficient to satisfy all human wants. It is the fundamental economic problem and cannot be solved — it can only be managed.

A shortage is different. A shortage occurs when demand for a specific good exceeds its supply at a given price. Shortages can be resolved by adjusting prices; scarcity, arising from unlimited wants against finite resources, cannot.

Because resources are scarce, every decision to use them one way means giving something else up. This is the idea of opportunity cost: the value of the best alternative that must be sacrificed when a choice is made.

Example

A student has $2,000 and must choose between buying a phone or textbooks. If she buys the phone, the opportunity cost is the textbooks she could have had instead. If she buys the textbooks, the opportunity cost is the phone.

A government allocates $500 million to build a new highway. The opportunity cost might be the hospitals, schools, or tax cuts that could have been provided with the same funds.

Remember

Opportunity cost is not money spent — it is the value of what you give up. Even "free" decisions have opportunity costs because time and effort are scarce.

Free Goods vs Economic Goods

| Type | Definition | Examples |

|---|---|---|

| Free goods | Available in unlimited supply; have no opportunity cost | Air, sunlight, seawater |

| Economic goods | Scarce; obtaining them requires giving something up | Food, clothing, land, labour |

In practice, goods that were once free (clean air, fresh water) can become economic goods when pollution or overuse makes them scarce.

The Three Economic Agents

An economy is a system that organises resources to produce goods and services and distribute them to satisfy society's needs and wants. Three main groups of decision-makers operate within it:

Households own the factors of production (land, labour, capital) and supply them to firms in exchange for income. They then spend that income on goods and services. Households are both suppliers (of factors) and buyers (of products).

Firms hire factors from households and use them to produce goods and services. Their primary objective in a market economy is to maximise profit. Firms are both buyers (of factors) and sellers (of products).

Government collects taxes and uses the revenue to provide public goods, regulate markets, redistribute income, and pursue macroeconomic goals like full employment and price stability. Government can act as both a producer (running public enterprises) and a buyer (purchasing goods and services).

Factors Affecting Economic Decisions

Each agent's decisions are shaped by:

- Prices and costs

- Availability of income and credit

- Expectations about the future

- Laws and regulations

- Cultural norms and preferences

- Technology

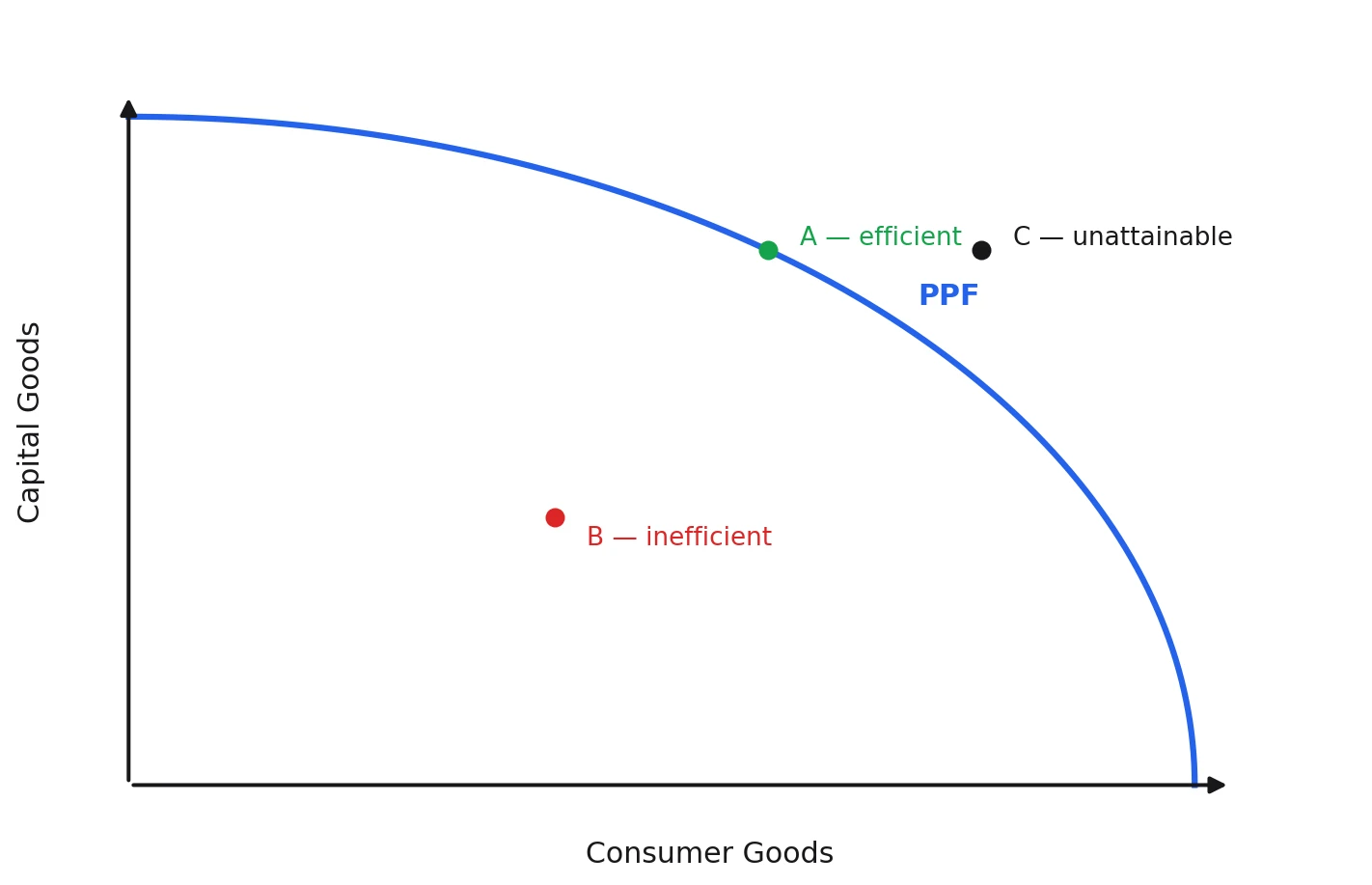

The Production Possibility Frontier

The production possibility frontier (PPF) is a curve showing all the combinations of two goods that an economy can produce when it is using all its resources fully and efficiently. Every point on the curve represents a maximum output combination given current resources and technology.

Reading the PPF

A point on the curve is productively efficient — all resources are fully employed and there is no waste.

A point inside the curve is inefficient — some resources are unemployed or misallocated. During a recession, the economy operates inside its PPF.

A point outside the curve is currently unattainable — the economy does not have enough resources or technology to reach it.

Opportunity Cost on the PPF

Moving along the curve from one combination to another shows opportunity cost directly. To produce more of one good, some of the other must be sacrificed. The bowed-out (concave) shape of the PPF reflects the law of increasing opportunity costs: as more of one good is produced, the opportunity cost of each additional unit rises because resources are not perfectly suited to every use.

Exam Tip

A straight-line PPF implies constant opportunity costs — resources are equally suited to producing either good. A bowed-out (concave) PPF implies increasing opportunity costs — the more realistic case.

Shifts of the PPF

The entire curve shifts outward when the economy's productive capacity increases. The main causes:

- Discovery of new natural resources (e.g., oil deposit found)

- Improvement in technology — more output from the same inputs

- Growth in the labour force — more workers available

- Increase in capital stock — more investment in machinery and equipment

- Improved education and training — raising labour productivity

The curve shifts inward when capacity falls: natural disasters, war, emigration of skilled workers, or depletion of natural resources.

An outward shift specifically for one good only (e.g., only in the direction of capital goods) occurs when technological progress or resource discovery applies to that sector alone. The curve pivots rather than shifting uniformly.

Economic Growth, Efficiency, and the PPF

Productive efficiency is achieved at any point on the PPF — maximum output is squeezed from available resources.

Economic growth is an outward shift of the PPF itself, reflecting increased productive capacity over time.

A country that currently produces inside its PPF can move to the curve by reducing unemployment or waste. Moving the curve itself requires investment, innovation, or resource discovery.